What should be your debt investment strategy as the US Fed, RBI cut rates?

As the US Federal Reserve has reduced benchmark interest rates by 25 basis points and indicated additional rate cuts in the coming months, expectations have risen that the Reserve Bank of India (RBI) will follow suit and cut rates in its next policy decision on October 1.

After delivering a larger-than-expected 50 basis point rate cut in June this year, the RBI kept the repo rate unchanged at 5.5 per cent and maintained its policy stance as “neutral” in its August policy meeting.

With the start of the Fed rate reduction cycle, the RBI has the opportunity to cut rates and further accelerate India’s economic growth without worrying much about inflation and the rupee’s weakness.

Monetary easing lowers borrowing costs, boosts consumption, and tends to cause a rally in the stock market. This raises a pertinent question about what our debt investment strategies should be during rate reductions.

Rate cuts and bonds

Like equities, central banks’ rate reduction exercise affects the debt investment landscape, including government bonds, corporate debentures, and fixed-income mutual funds.

For equities, a rate reduction could mean the return of risk appetite, as borrowing costs are down, which increases the prospects of increased consumer spending and better corporate profitability.

However, for equities, it appears to be slightly complex.

Monetary easing could be both an opportunity and a challenge for debt investors. This is because there is an inverse relationship between interest rates and bond prices.

Bonds have a fixed interest rate, known as the coupon rate. When the rate is cut, newly issued bonds offer a lower coupon rate to reflect the new, lower interest rate environment.

So, during times of monetary easing, existing longer-duration bond prices rise as their fixed coupon rate becomes more attractive compared to new bonds at lower rates.

What does this do? It makes debt investors flock to buy existing old bonds, and this increased demand drives up the market price of old bonds. When bond prices go up, yields go down because bonds’ coupon payments are fixed.

For example, suppose you buy a ₹100 bond with a 10 per cent coupon rate. You’ll receive ₹10 as interest each year. If demand pushes the bond’s market price up to ₹110, you’ll still get only ₹10 interest because the coupon is fixed. At this higher price, your effective return (yield) drops to about 9.1 per cent. That is why we say bond prices and bond yields go in opposite directions. The higher the bond price, the lower the return and vice versa.

So, does this mean during times of rate cuts, you should stop debt investment?

Debt investment in times of monetary easing

Nikhil Aggarwal, the founder and group CEO of Grip Invest, says that with the Fed signalling further rate cuts, the RBI might follow suit to support growth and manage capital flows.

Lower rates translate into an increase in bond yields for fixed-income investors, creating an opportunity for Indian debt investors to position themselves ahead of the rate cut cycle.

“If we think about a rate cut environment, it usually means a steeper curve as the RBI has more control over the short term. The front end has already increased in prices due to RBI easing, and the reinvestment risk also comes into focus earlier in the shorter tenure end. It can be suitable for investors who are looking to move out of cash,” said Aggarwal.

“On the other hand, for longer tenure assets, you don’t get much extra yields as you are taking on a lot more tenure and potential volatility. Thus, mid tenure bonds across the rating curve would benefit the most from this. These can give you attractive yields, potential price gains if RBI rates fall and a long runway for consistent returns,” said Aggarwal.

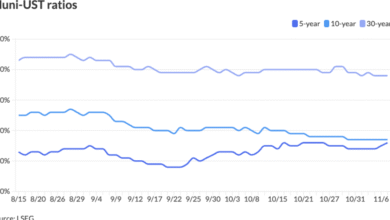

Murthy Nagarajan, the head of fixed income at Tata Mutual Fund, underscored that the Indian Government and the RBI are working to lower the supply of long-dated papers due to reduced demand from insurance companies and the Employee Provident Fund Organisation (EPFO).

The spread between 10-year and 40-year government securities has increased to 80 basis points, which should reduce in the coming months. Investors may invest in gilt funds and corporate bond funds due to their attractive carry and scope for capital appreciation in the coming months, said Nagarajan.

Abhishek Bisen, Senior EVP and fund manager of fixed income at Kotak Mutual Fund, believes the RBI may also ease rates after the US Fed cut its benchmark rate by 25 bps and hinting at further reductions.

In this context, the Indian yield curve remains steep, with longer-term yields relatively high despite strong macro fundamentals as compared to other economies.

According to Bisen, this suggests that long-duration bonds are undervalued, presenting opportunities for investors.

“We recommend greater allocation to sovereign bonds at the long end of the curve, benefiting from potential capital appreciation if yields fall. However, debt investors should consider asset allocation based on their risk appetite, return objectives, investment horizon, taxes, legal factors, liquidity needs, and any other unique constraints,” said Bisen.

Read more stories by Nishant Kumar

Disclaimer: This story is for educational purposes only. The views and recommendations expressed are those of individual analysts or broking firms, not Mint. We advise investors to consult with certified experts before making any investment decisions, as market conditions can change rapidly and circumstances may vary.

Credit: Source link