Will the ‘Japanese government bond storm’ sweep through the market again? European asset management giant bets on 30-year yields breaking above 3.5%.

Following the inauguration of Sanae Takichi, concerns over Japan’s fiscal discipline have intensified in the market; Amundi, Europe’s largest asset management giant, forecasted that yields on Japan’s long-term government bonds could reach new highs due to fears that the new Japanese prime minister would increase borrowing.

According to Zhitong Finance, a recent research report released by Amundi, Europe’s largest asset management firm, indicated that yields on Japanese government bonds with longer maturities might hit new historical highs in the coming months due to concerns about significant borrowing by Japan’s newly appointed prime minister. If yields on Japanese government bonds with long maturities (10 years or more) rise sharply in a short period, the ‘Japanese bond sell-off storm’—which once triggered brief collapses across global equity, bond, and currency markets—might strike global financial markets again.

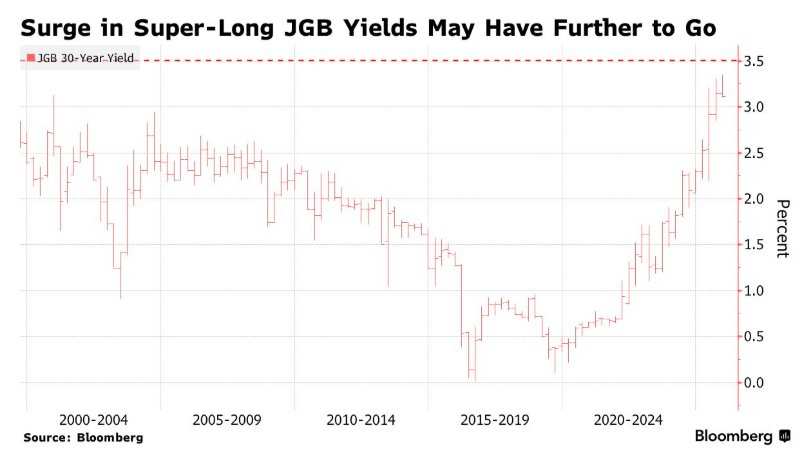

Claire Huang, Senior Macro Strategist for Emerging Markets at Amundi Investment Institute, stated that the yield on Japan’s 30-year government bonds could significantly rise above 3.5% for a period, implying an increase of nearly 40 basis points from Wednesday’s trading levels.

Sanae Takichi was elected as Japan’s prime minister on Tuesday after forming a new coalition government. She has long advocated boosting domestic economic growth through increased government spending and supports maintaining a prolonged low-interest-rate monetary policy stance.

Is ‘Abenomics’ making a comeback?

Takaichi, aged 64, is a conservative nationalist who lists former British Prime Minister Margaret Thatcher as one of her role models. She has long been an ally of Japan’s longest-serving prime minister, the late Shinzo Abe, and a staunch follower of his policies, which is why financial markets are beginning to bet that ‘Abenomics’ will make a comeback.

The so-called “Sanae Trade,” which has recently gained significant attention globally, refers to financial market expectations following the victory of Sanae Takaichi, the new president of Japan’s Liberal Democratic Party. These expectations are centered around the reinstatement of policies akin to “Abenomics”—namely, actively promoting an “ultra-loose fiscal framework” while maintaining a cautious stance toward monetary tightening—which have triggered sharp fluctuations across stock, bond, and currency markets. The “Sanae Trade” is primarily reflected in a swift surge in Japan’s stock market, continued depreciation of the yen, and the resumption of the “yen carry trade.” Therefore, betting on the “Sanae Trade” essentially equates to wagering on a Japanese reflationary mix of stronger fiscal stimulus, industrial support, and accommodative monetary policy—going long on Japanese equities, shorting the yen, and avoiding long-duration assets.

‘There are concerns about fiscal discipline, especially in the medium term,’ said Claire Huang, who focuses on investment strategies for Asian countries. ‘I wouldn’t say the outlook for Japan’s ultra-long-dated bond yields is particularly optimistic, or that the selloff in long-term debt has completely ended.’

Market expectations for the Bank of Japan’s interest rate hikes are heating up, and political and fiscal policy uncertainties are keeping long-term Japanese government bond yields persistently high. Earlier this month, the 30-year Japanese government bond yield reached 3.345%, marking the highest level for this long-term sovereign bond since its issuance in 1999. Japanese long-term government bonds have been among the worst-performing sovereign assets globally this year.

Strategist Claire Huang expects that investors may only return to longer-duration Japanese government bonds when Masako Takahashi’s economic and fiscal policies become clearer and she is able to control the rising cost of living in Japan.

Although she has ordered a new package of economic measures aimed at easing the burden of inflation on Japanese households and businesses, the Takahashi administration has not specified the scale of the plan or whether it will require additional large-scale issuance of long-term government bonds to finance it.

The ‘Term Premium’ Effect

While slowing inflation may curb the rise in ultra-long-term yields, Claire Huang noted that there remains upside risk for the 10-year Japanese government bond yield to reach 1.8%. This scenario could occur as the Bank of Japan gradually reduces its substantial inventory of bonds accumulated under its Yield Curve Control (YCC) policy.

Since the beginning of this year, long-term government bond yields in developed markets globally have surged continuously. With some of the world’s largest central banks issuing new warnings about fiscal spending, expanding debt servicing, and declining demand for long-term bonds, the likelihood of a historic 3.5% increase in 30-year Japanese government bond yields has grown under the combined influence of Masako Takahashi’s “Abenomics” policy framework and the impact of the ‘term premium’.

The term premium refers to the additional yield compensation investors demand for holding long-term bonds. This phenomenon has been particularly pronounced in the U.S. Treasury market, where the term premium has consistently hovered near a decade-high since the start of this year.

In the view of some economists, government debt and budget deficits during Trump 2.0 are likely to be much higher than official projections, primarily due to the new administration’s growth and protectionist framework centered on ‘domestic tax cuts + external tariff hikes.’ Coupled with growing budget deficits, rising U.S. Treasury interest payments, and increased defense spending, the U.S. Treasury may be forced to expand issuance even further compared to the Biden administration’s already high levels. Additionally, amid de-globalization trends, potential significant reductions in U.S. Treasury holdings by China and Japan, along with spillover risks from rising Japanese government bond yields, suggest that the term premium will likely rise significantly above historical averages. This partly explains why the 10-year U.S. Treasury yield, often referred to as the ‘global asset pricing anchor,’ has remained above 4% for much of this year.

Regarding the yen—which fell sharply by approximately 2.5% this month amid market concerns that Masako Takahashi might hinder the Bank of Japan’s interest rate hike process—strategist Claire Huang expects that a weaker sovereign currency will actually strengthen the case for rate hikes by the Bank of Japan, as more expensive imports would significantly increase domestic inflationary pressures.

“If USD/JPY breaks through 155 and sustains trading within the 155–160 range, the Bank of Japan is likely to continue raising rates,” she emphasized. After the yen exchange rate (USD/JPY) briefly fell to around 153 per dollar earlier in October, hitting an eight-month low, this level is now close at hand. At 7:10 AM Tokyo time on Thursday, the yen was trading at 151.84. Claire Huang stated that whether further rate hikes occur this year ultimately “depends on the yen.”