U.S. market outlook: Embracing the certainty of uncertainty

Equity markets in Europe and Canada were also bolstered by expanded domestic fiscal spending to countervail the negative impacts of tariffs, and by interest rate cuts from their central banks.

U.S. investors also found cause for more optimism when they turned their attention toward the prospects of business-friendly tax and regulatory policies laid down for 2026 as the “one big beautiful bill” passed into law.

Recognition that changes to trade and labour policies could manifest into higher inflation, the U.S. Federal Reserve left interest rates unchanged until September. Weighing their dual policy mandate of price stability and full employment, Chairman Powell and the Federal Open Market Committee (FOMC) were contending with an uncertain inflation transmission mechanism. How much of the U.S. tariff increases would businesses pass through to consumers?

Inflation remained relatively stable in the summer, but it was the labour market that eventually showed cracks and this pushed Powell and the FOMC to cut rates by 0.25% in September.

In the lead up to that rate decision, President Donald Trump’s power politics had potentially thrown in doubt the future independence of the Federal Reserve. His effort to remove Federal Reserve governor Lisa Cook from her position — currently under review by the courts — has been widely interpreted as a significant step toward establishing informal control of monetary policy from the executive branch.

Politics has traditionally been relegated to the fringe of Federal Reserve governance through the appointment of the chair of the FOMC. President Trump has pushed politics to the heart of the Fed by voicing his almost continuous displeasure with the high level of interest rates, the unprecedented attempt to remove Governor Cook and by installing Stephen Miran as an interim Federal Reserve governor to fill a vacant seat just days before the September FOMC meeting.

Miran dissented in favour of a 0.50% rate cut at the meeting, and was almost certainly the outlier governor who projected the need for 1.50% in cuts by the end of 2025.

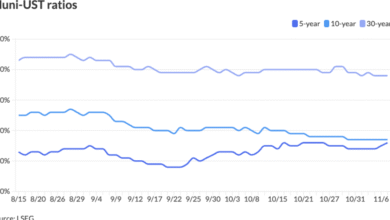

The politicization of the Fed and the potential loss of monetary policy credibility is a looming wildcard for markets. In recent weeks, the bond market has begun to discount a modest rise in inflation expectations and the long end of the U.S. Treasury yield curve has steepened.

Estimates of second quarter U.S. GDP growth were increased, showing that consumers are still willing and able to drive economic growth. Labour markets are distinctly softer, however, reflecting genuine economic uncertainty since the beginning of the year. This is despite U.S. businesses looking ahead at 2026 to accelerate capital spending, encouraged by accounting policy inducements and the promise of productivity from AI technologies.

If we see a continuation of firming economic data, with core inflation hovering uncomfortably near the 3% level, the expectations of another 1% in rate cuts over the next year may need to be reconsidered.

Hiccups ahead?

There are several other significant U.S. domestic and international policy event risks on the horizon that could cause hiccups for markets. There are many, varied legal challenges to the status quo under way in the U.S. that have potential ramification to which sectors and companies may have to adapt. The timing and clarity of U.S. Supreme Court decisions are to be determined.

Geopolitical tensions remain high regarding regional conflicts, now buffeted by ongoing back-and-forth shifts in U.S. leadership and support for stability afforded by decades-old institutions such as NATO and the UN. And, in just about 12 months from now we will be waist-deep in the U.S. midterm elections.

Investors seem to be approaching this diverse mix of inconsistent indicators and policy-event risks with a glass-half-full mentality. Stock markets in many regions have set new highs and index valuations can appear somewhat stretched.

Beneath the familiar index heavyweight names, however, investors can find some more fairly-valued equity opportunities. Corporate bond spreads have narrowed and financial conditions have remained supportive of funding generally, even though there has been a drift higher in default rates driven by weaker credits. Support for equity and bond market strength reflects the prevailing view that earnings growth has been solid. With potential interest rate cuts ahead, investors should remove recession worries from their minds.

Nevertheless, with market volatility low and risk premiums in many markets at their lowest levels of the year, a neutral equity-bond asset mix and increased portfolio diversification are recommended. For portfolios that have leaned heavily on large-cap exposures, particularly in the U.S., adding to small- or-mid cap holdings, or international equities, could help to diffuse that concentration and balance exposures through the months of uncertainty ahead.